Looking Beneath the Numbers: Assessing Pakistan's FY2026 Growth Performance

Prime Comment #36

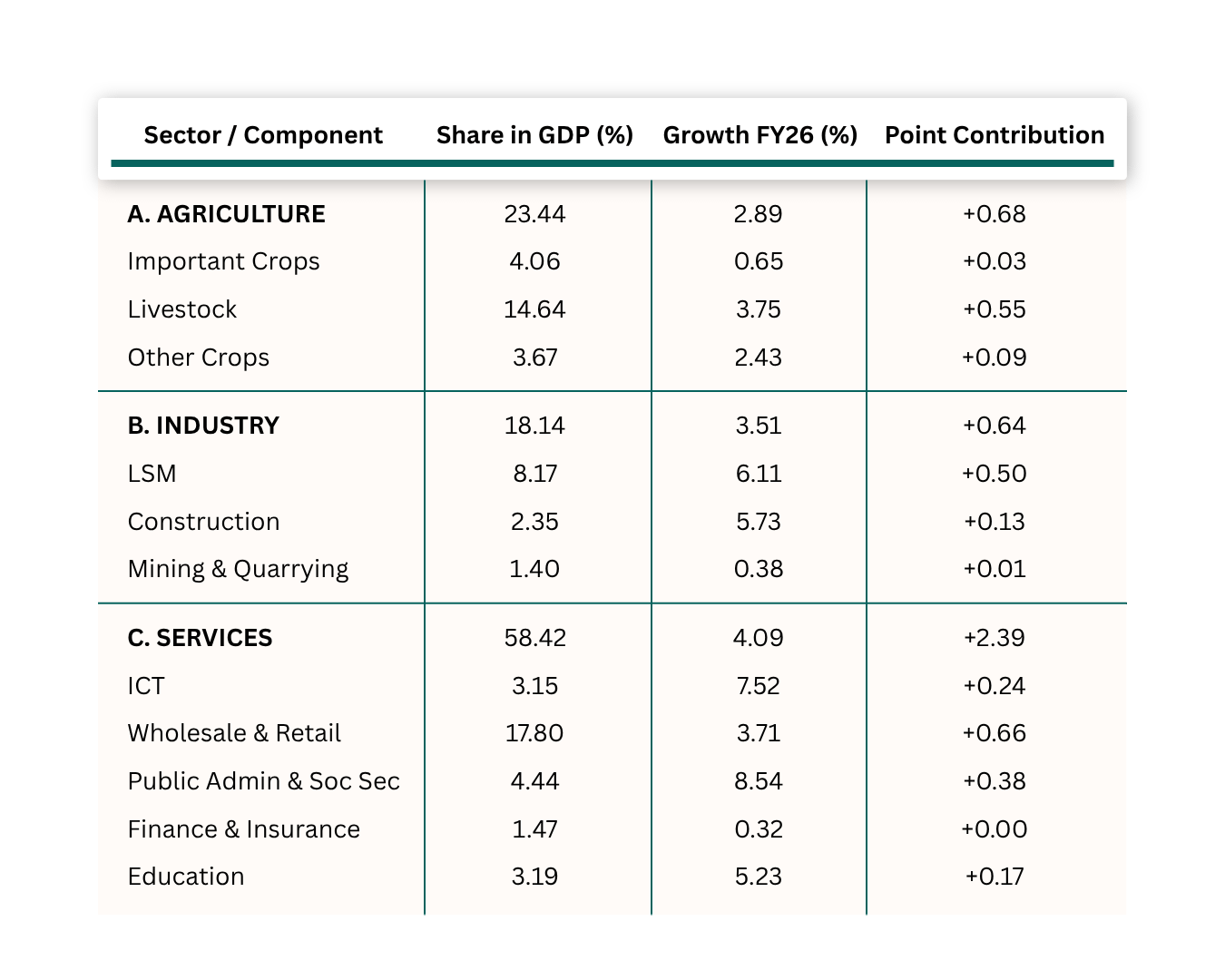

Pakistan’s GDP grew by 3.70% in FY2026, compared with 3.18% in FY2025, supported by major economic sectors. Agriculture grew by 2.89%, driven by livestock and crops at 3.75% and 1.44%. The industrial sector grew by 3.51%, supported by a sharp increase in Large-Scale Manufacturing (LSM) by 6.11%. The services sector, which accounts for 58.42% of GDP, grew by 4.09%, led by information and communication services at 7.52%. In terms of point contribution, agriculture contributed 0.68, industry 0.64 and services 2.39.

While the headline growth number is encouraging, a closer look at the composition reveals a mix of significant developments and deep structural vulnerabilities that the aggregate number conceals. On the positive side, large-scale manufacturing rebounded sharply to 6.11% after contracting 0.69% last year, with broad sub-sectoral participation; automobiles grew by 61.7%, petroleum products 10.9%, food 9.8%, and rubber 14.3%. However, the contraction in pharmaceuticals (-5.14%) and machinery & equipment (-8.72%) indicates that higher-value-added segments remain under stress. The information and communication sector grew by 7.52%, while IT remittances grew 19.8% to $3.38 billion and freelancer exports increased by 51%. This is sustainable, productivity-driven growth in a high-value sector with real long-term potential. Private investment grew 12.8%, exceeding public investment at 11.6%, indicating increased business confidence and a positive shift toward market-led capital formation. In the agriculture sector, livestock is the backbone of rural livelihoods for almost over 8 million families, increasing from 2.95% to 3.75%, directly supporting lower-income rural households. The construction sector maintained a robust growth of 5.73%, generating employment for unskilled labour. The structural concerns, however, are equally significant. Consumption accounts for 93.6% of GDP, while saving 14.13% and investment 14.38% remain lowest in the region. The energy utilities sector contracted by 10.63%, due to the rapid adoption of rooftop solar, which has shifted consumption away from the grid, a structural transition the Survey does not account for. The $72 million current account surplus is nearly completely based on $30.3 billion in worker remittances; without remittances, Pakistan would run a deficit more than 5% of GDP. In agriculture, significant crops rose by only 0.65%, with cotton and maize both decreasing, resulting in rural income stagnation for the 37.4% of the labour population that is employed in agriculture. Public Administration and Social Security grew 8.54%, faster than ICT (7.52%), education (5.23%), or health (6.85%). In an economy undergoing IMF-mandated rightsizing of government, a trajectory internally inconsistent with the IMF-mandated reform narrative, given that growth driven by expanding bureaucratic output carries low productivity multipliers. Underlying all these concerns is the investment-to-GDP ratio of 14.38%, the lowest among all major Asian economies. At this level, with a conservative ICOR of 3.5, Pakistan is arithmetically confined to grow at 3-4% per year, resulting in just 1.5-2% real per capita income growth after accounting for population increase. Until the savings-investment gap is structurally addressed, Pakistan’s development will be cyclical stabilisation rather than structural transformation.